If you’ve been told “Medigap is expensive,” you’ve been told a half-truth.

Medigap premiums in the United States span a range that dwarfs most insurance categories. Two 65-year-olds, on the same letter plan, in the same state, can pay premiums that differ by two or three times depending on which insurer they pick and how that insurer prices Medigap. That spread isn’t a quirk. It’s the central feature of how this market works — and the reason most adult children helping a parent shop for Medigap leave a lot of money on the table without realizing it.

This post is the version of the conversation you’d have with someone who’d already shopped Medigap for two parents and a stepparent. What Medigap actually is. The pricing structures that drive premium variation. What the average premium really tells you. And how to shop in a way that keeps your parent’s premium reasonable for the long haul.

Medigap in plain language.

Medigap (also called Medicare Supplement Insurance) is private insurance that pays the gaps Original Medicare leaves behind — the deductibles, coinsurance, and copays that Parts A and B require the patient to pay out of pocket.

Medigap is only for people on Original Medicare (Parts A and B). It does not work with Medicare Advantage. If your parent has Medicare Advantage, they cannot also have Medigap. If they want Medigap, they need to be on Original Medicare.

Medigap is sold by private insurers but the plans themselves are federally standardized. A “Plan G” from Insurer A and a “Plan G” from Insurer B cover exactly the same things. The difference is the premium and the customer service. This is the central insight of Medigap shopping: identical coverage, different prices.

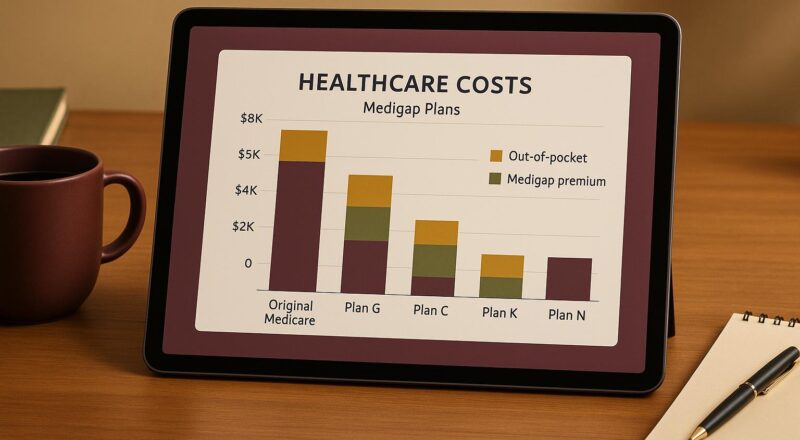

The standardized plan letters.

There are ten standardized Medigap plans, identified by letter: A, B, C, D, F, G, K, L, M, N. (Massachusetts, Minnesota, and Wisconsin have their own standardized systems; the rest of the country uses these ten.)

Two important changes:

- Plans C and F are no longer sold to new enrollees who became eligible for Medicare on or after January 1, 2020. People already enrolled in C or F before that date can keep them.

- Plan G is the most popular Medigap plan for new enrollees — it covers everything Plan F covered except the Part B deductible, which the enrollee pays out of pocket once a year (around $257 in 2025).

- Plan N is a popular lower-premium alternative to Plan G — it covers most of the same things but adds small copays for some doctor visits and emergency-room trips, and it doesn’t cover Part B excess charges.

For most adult children helping a parent shop, the realistic choice is between Plan G and Plan N, with a smaller minority looking at high-deductible Plan G or the lower-premium Plans K, L, or M.

Why two identical plans cost very different amounts.

Three pricing methods determine how Medigap premiums grow over time. Insurers in the same state can use different methods, which is the single biggest source of premium variation between insurers offering the same letter plan.

- Community-rated (also called no-age-rated): Everyone pays the same premium regardless of age. Premiums increase only because of inflation, not because the policyholder is getting older. Lowest long-term cost trajectory in many cases — but the entry premium is higher than other methods at age 65.

- Issue-age-rated: Premium is based on the age your parent first bought the policy. If they bought at 65, they keep the 65-year-old rate (with inflation increases). Premiums don’t go up because of age. Good middle-ground — locks in age-65 pricing.

- Attained-age-rated: Premium is based on your parent’s current age and goes up every year as they get older — on top of inflation increases. Lowest premium at age 65 of the three methods. Highest premium at age 80.

Most Medigap policies sold today are attained-age-rated. It’s the structure that looks cheapest when your parent first signs up. It’s also the structure that gets dramatically more expensive over time. Adult children helping a parent enroll often default to whichever insurer quoted the lowest premium without realizing the premium will compound aggressively for the next 20 years.

The extra ten or fifteen dollars a month for an issue-age-rated or community-rated plan often saves thousands over the life of the policy. Ask the agent which pricing method each plan uses. It’s often not on the comparison page.

What “the average Medigap premium” actually tells you.

National averages for Plan G typically run $120–$220 per month for a 65-year-old, but that average obscures more than it reveals. Real-world pricing in the same zip code, same plan letter, same age, can range from about $90 to $300 depending on insurer.

The factors that move premiums:

- State. Big variation between states. Florida, New York, and California tend to run high. Hawaii, Iowa, and several Midwestern states tend to run lower.

- Insurer. Within the same state, premiums for identical plans can differ 50% or more between insurers.

- Age. Attained-age-rated plans get more expensive every year.

- Gender. In most states, women pay slightly less for Medigap than men do at the same age. (A few states ban gender-based pricing; check your state.)

- Tobacco use. Tobacco users pay 10–25% more in most states.

- Household discount. Many insurers offer a 5–12% discount when both spouses have Medigap with the same insurer. Worth asking about — easy to miss.

- Underwriting. Inside the open enrollment window, your parent’s health doesn’t affect the premium. Outside it (more on that below), insurers can charge more or refuse coverage.

The one number that means more than the average premium: the spread between the highest and lowest premium in your parent’s state for the same plan. That’s the savings on the table.

The Medigap Open Enrollment Period. The single most important window.

When your parent first enrolls in Medicare Part B at age 65 or older, they have a six-month Medigap Open Enrollment Period. During that window:

- They can buy any Medigap plan available in their state from any insurer

- The insurer cannot use medical underwriting (cannot charge more or refuse coverage based on health)

- This is the one time the entire Medigap market is open to them on equal terms

After the six months close, in most states, insurers can use medical underwriting. They can charge more, exclude pre-existing conditions, or decline to sell a policy at all. A parent with diabetes, atrial fibrillation, cancer history, or other common conditions may find Medigap unavailable or unaffordable later.

A few states have stronger protections — Connecticut, Massachusetts, Maine, New York, and a handful of others have year-round guaranteed-issue rights or other Medigap protections. In most states, the Open Enrollment Period is the only window where your parent can shop without underwriting. Skipping it because your parent feels healthy at 65 is a decision that affects their options at 80.

Why premiums rise. And how to plan for it.

Even on a community-rated or issue-age-rated plan, premiums rise. The drivers:

- Medical inflation. Healthcare costs rise faster than general inflation. Medigap premiums rise with them.

- Aging into a higher-cost state, if relevant. Plans aren’t portable; if your parent moves to a higher-cost state, premiums change.

- Insurer rate filings. Insurers periodically file rate increases with state regulators. Even community-rated plans see increases.

A reasonable expectation is 3–8% annual premium increases for most Medigap policies, occasionally higher in high-utilization years. Over a 20-year retirement, the trajectory of premium increases compounds — which is why the choice of pricing method (community vs. issue-age vs. attained-age) matters more than it appears at the moment of enrollment.

How to shop Medigap well.

Six things that matter more than the marketing materials:

- Use Medicare’s Plan Finder — the official comparison tool at Medicare.gov. Lists all Medigap plans available in your zip code, all insurers, all premiums.

- Sit with a SHIP counselor. Free, unbiased, and they’ll walk through plan letters, pricing methods, and insurer histories with you. (Find your state SHIP.)

- Ask each insurer which pricing method they use. Community-rated, issue-age-rated, or attained-age-rated. Often not on the brochure.

- Ask about household discounts. 5–12% off if both spouses enroll. Often not mentioned proactively.

- Look at the insurer’s rate increase history, not just the current premium. State insurance departments publish this; ask your SHIP counselor for guidance.

- Buy during the Open Enrollment Period. The six months starting when your parent enrolls in Part B at 65 or older. Underwriting-free. Don’t skip this window.

“Identical coverage, different prices. Two 65-year-olds on the same Plan G in the same state can pay premiums that differ two or three times. That spread isn’t a quirk — it’s the central feature of how this market works.”

FROM WATCHING THE OPEN ENROLLMENT WINDOW MATTER:

Of all the Medicare-related things I learned across fifteen years of helping parents and stepparents through this system, the one I’d most want to put on a billboard is this: the Medigap Open Enrollment Period is a six-month window, and most adult children don’t know it exists until it’s already closed.

The version of this story that plays out in countless families is the same: parent turns 65, picks a Medicare Advantage plan because the premium looks lower, feels fine for a decade, then around 75 or 78 a serious diagnosis arrives, and suddenly they want the broader provider access of Original Medicare with Medigap. That’s the moment they discover that getting a Medigap policy in their state, with their now-existing health conditions, is either dramatically more expensive or simply not offered.

The choice they made at 65 — feeling young, feeling healthy, feeling like the cheaper plan made sense — locked them into the path they’re now stuck with.

What I wish more adult children knew, and what I’d want every family I work with to know going into Medicare eligibility: the Medigap Open Enrollment Period is a one-time gift from the system. Six months, no medical underwriting, every plan available on equal terms. Use it, even if your parent feels healthy. A modestly priced Plan G or Plan N during that window is insurance against the version of your parent’s life ten years from now, when health is more complicated and the underwriting door has closed.

Honor is in the name of our company for a reason: ElderHonor. Honoring our parents includes building the financial structure that gives them options when their needs change — not just the cheapest option at 65. The pricing-method choice (community-rated vs. attained-age-rated) and the open-enrollment timing are the two leverage points that determine whether your parent has Medigap at 80 — and whether they can afford it.

The version of this post if I had to pick.

If your parent is approaching 65 and choosing between Original Medicare + Medigap and Medicare Advantage, this is the version of the math that matters:

- The premium difference between MA and Original Medicare + Medigap is real — but smaller than the brochure suggests once you add Part D and account for prior-authorization risks on the MA side.

- The pricing-method decision (community-rated vs. attained-age-rated) is more consequential than most agents emphasize.

- The Open Enrollment window is non-renewable. If your parent doesn’t enroll in Medigap during their first six months on Part B, in most states, they may never be able to get it on the same terms again.

Use the SHIP counselor. Use Medicare.gov’s Plan Finder. Ask the right questions. The Medigap market rewards the families who shop carefully — sometimes by thousands of dollars a year, every year, for the rest of their parent’s life.

You’ve got this.

The toolkit’s Documents and Roadmap modules walk through the Medicare enrollment timeline, the doctor-and-medication worksheet, and the annual review cadence — built so the Medigap decision is made well the first time and reviewed appropriately year over year.

Some additional articles that might be helpful:

- The Pros and Cons of Medicare Advantage vs. Original Medicare — already linked inline; foundational read for the choice that surfaces Medigap

- The Medicare vs Medicaid: Understanding Dual Eligibility — relevant for dual-eligible readers (who don’t typically need Medigap because Medicaid covers cost-sharing)

- The Medicare and Long-Term Care: What Families Should Know — companion piece for what Medicare doesn’t cover (and what Medigap can’t help with either)

- Resource Library — specifically SHIP, Medicare.gov Plan Finder

Some additional notes:

Premium ranges ($120–$220/month for Plan G; spread of $90–$300 in same zip code) are illustrative. The most current data should come from Medicare.gov Plan Finder.

The Part B deductible figure (~$257 in 2025) changes annually. Verify against the current year’s Medicare.gov costs page.

The state-specific Medigap protections list (CT, MA, ME, NY, plus a handful of others) is approximate and changes periodically as states pass legislation. Verify the current state-by-state landscape at the National Association of Insurance Commissioners or via your state SHIP.

The 3–8% annual premium increase range is a reasonable historical estimate but premium trends shift over time. This is not a guarantee, validate it before making any decisions.

The “Plan C and F no longer sold to new enrollees” rule is stable federal policy from MACRA (effective January 1, 2020). This may change so verify before making any decisions.

Back to the Caregiver Library. Read more on Money, Medicare & legal.