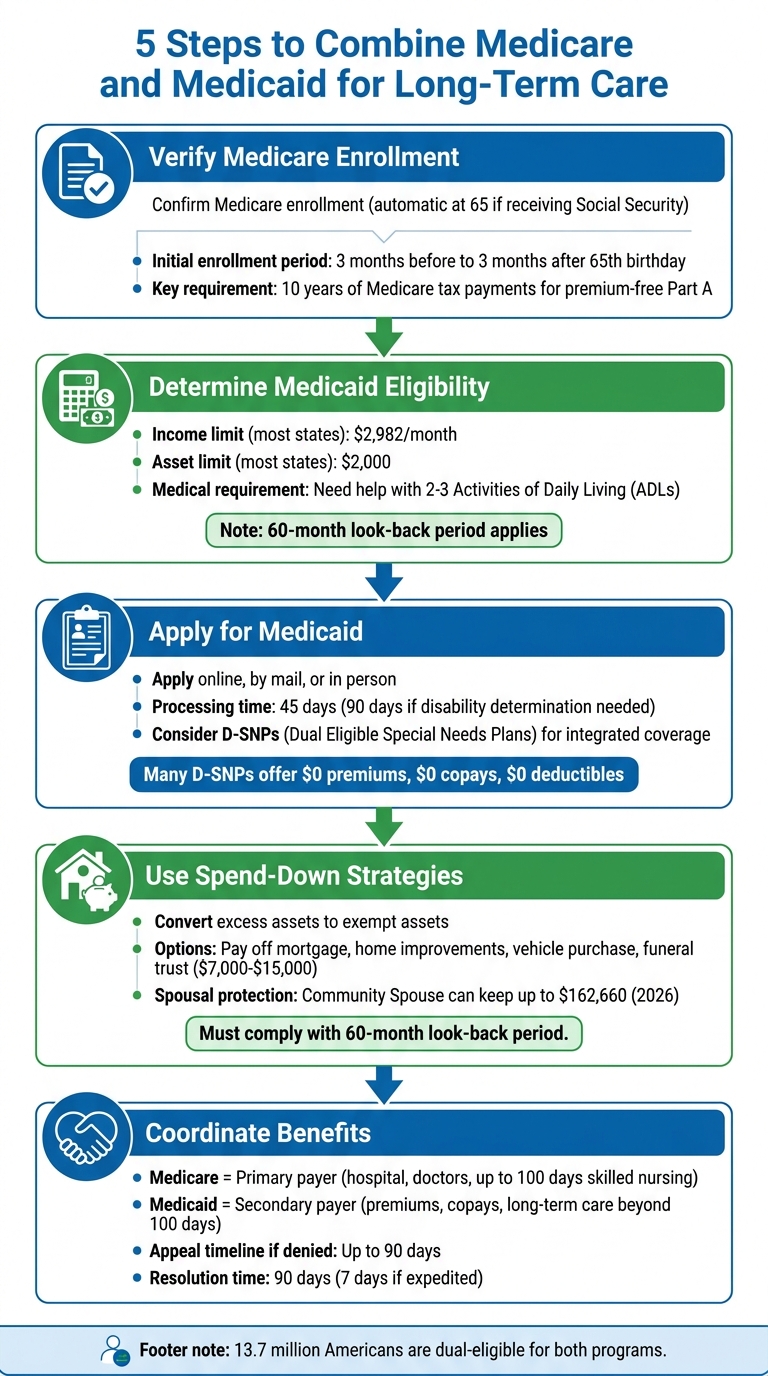

Navigating long-term care costs can be overwhelming, especially when Medicare doesn’t cover extended nursing home stays or daily personal care. Combining Medicare and Medicaid can help bridge this gap, but the process requires careful planning. Here’s a quick breakdown of the five steps to coordinate these benefits:

- Step 1: Confirm your parent’s Medicare enrollment to ensure coverage is in place.

- Step 2: Check Medicaid eligibility, including income and asset limits, which vary by state.

- Step 3: Apply for Medicaid and explore options like Dual Eligible Special Needs Plans (D-SNPs) to simplify benefit management.

- Step 4: Use legal spend-down strategies to meet Medicaid’s strict financial criteria without penalties.

- Step 5: Handle approvals, appeals, and coordinate Medicare and Medicaid benefits for seamless coverage.

5 Steps to Combine Medicare and Medicaid for Long-Term Care

Medicare vs. Medicaid: Understanding dual eligibility

sbb-itb-48c2a85

Step 1: Verify Medicare Enrollment and Eligibility

Start by confirming your parent’s Medicare enrollment to ensure Medicaid can act as the secondary payer without any coverage gaps.

If your parent is already receiving Social Security or Railroad Retirement Board (RRB) benefits, they’ll be automatically enrolled in Medicare Parts A and B on the first day of the month they turn 65. About three months before their 65th birthday, they should receive a welcome package and their Medicare card in the mail. Another way to confirm enrollment is by checking their Social Security statements to see if the Part B premium is being deducted.

For parents not yet receiving Social Security benefits, you’ll need to apply for Medicare manually. This can be done by visiting socialsecurity.gov, calling 1-800-772-1213, or visiting a local Social Security Administration (SSA) office. Applying during the initial enrollment period – three months before and after their 65th birthday – is crucial to avoid late penalties and delays in coverage.

Who Qualifies for Medicare

Medicare eligibility generally begins at age 65. However, younger individuals may qualify under specific circumstances, such as receiving Social Security Disability Insurance (SSDI) for at least 24 months, having End-Stage Renal Disease (ESRD), or being diagnosed with Amyotrophic Lateral Sclerosis (ALS, also called Lou Gehrig’s disease).

To qualify for premium-free Part A, your parent (or their spouse) must have worked and paid Medicare taxes for at least 10 years. Part B, on the other hand, requires a monthly premium, which may increase based on income. If the minimum work history isn’t met, Part A can still be purchased, though it will come with additional costs.

How to Enroll in Medicare

Parents receiving Social Security or RRB benefits don’t need to take any action – they’re automatically enrolled in Medicare Parts A and B. For everyone else, manual enrollment is required during the Initial Enrollment Period. This period begins three months before their 65th birthday and extends three months after. Applications can be submitted online at socialsecurity.gov, by calling 1-800-772-1213, or in person at a local SSA office.

When applying, make sure to have these documents ready: your parent’s birth certificate, proof of U.S. citizenship or legal residency, and work history. To estimate costs and confirm eligibility timing, use the Medicare Eligibility Tool at Medicare.gov. Additionally, for free guidance, reach out to the State Health Insurance Assistance Program (SHIP) at 1-877-839-2675.

“If you already get benefits from Social Security… you are automatically entitled to Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) starting the first day of the month you turn age 65.” – HHS.gov

Once you’ve confirmed Medicare enrollment, the next step is to check Medicaid eligibility for long-term care support.

Step 2: Determine Medicaid Eligibility for Long-Term Care

After confirming Medicare enrollment in Step 1, the next step is to assess if your parent qualifies for Medicaid’s long-term care services. Unlike Medicare, Medicaid eligibility depends on meeting specific financial and medical criteria, which vary by state.

Income and Asset Limits

For 2026, many states set the monthly income limit for Nursing Home Medicaid and Home and Community Based Services (HCBS) Waivers at $2,982, with an asset limit of $2,000 per individual. However, these thresholds aren’t uniform. For example:

- Illinois: Income limit is $1,304/month.

- California: No income limit for nursing home coverage.

- Connecticut: Asset limit is $1,600.

- California: Asset limit is $130,000 for an individual ($195,000 for married couples).

- New York: Asset limit is $33,038 for an individual ($44,796 for married couples).

Some assets, such as a primary home (within equity limits ranging from $752,000 to $1,130,000, depending on the state), one vehicle, wedding rings, and essential household furniture, are considered exempt. Non-exempt assets include bank accounts, stocks, bonds, and retirement accounts.

If your parent’s income exceeds the state threshold, explore whether your state offers a “Medically Needy Pathway.” This option allows excess income to be spent on medical bills to meet Medicaid requirements. In states without this option, setting up a Qualified Income Trust (QIT) or Miller Trust may be necessary to manage excess income.

Medical Requirements for Long-Term Care

Meeting financial criteria is only part of the equation. Your parent must also demonstrate a medical need for long-term care. This is typically determined through a Nursing Facility Level of Care (NFLOC) assessment. The evaluation focuses on your parent’s ability to perform essential Activities of Daily Living (ADLs), such as:

- Mobility

- Bathing

- Dressing

- Eating

- Toileting

Each state has its own criteria, but assistance with at least two or three ADLs is often required. A state-appointed nurse or social worker usually conducts the assessment, working alongside your parent’s primary care provider to confirm medical needs. Conditions like Alzheimer’s disease are considered but do not automatically qualify someone for NFLOC. It’s crucial to ensure that medical records clearly document any limitations, such as difficulty transferring, incontinence, or eating.

This evaluation determines whether your parent qualifies for nursing home care or if they can receive services at home through HCBS Waivers.

Understanding Your State’s Medicaid Rules

Since Medicaid is state-administered, the rules for long-term care coverage can vary widely. Start by identifying the Medicaid category your parent fits into – such as Nursing Home Medicaid, HCBS Waivers, or Aged, Blind, and Disabled (ABD) Medicaid – as each comes with its own benefits and regulations. To get state-specific application details, reach out to your State Medical Assistance Office or a local Aging and Disability Resource Center (ADRC).

Be aware of the 60-month look-back period, during which any asset transfers or gifts made in the past five years are reviewed. Transfers for less than fair market value during this time can result in a penalty, making your parent temporarily ineligible for Medicaid. To prepare, gather 60 months’ worth of financial records, including bank statements, tax returns, property deeds, and documentation of any gifts or transfers.

If your parent owns a home but plans to move into a care facility with the intention of returning later, filing an “intent to return home” statement can help keep the home classified as an exempt asset. Given the complexity of Medicaid rules – like spousal protections, home equity limits, and look-back regulations – it may be wise to consult a Certified Medicaid Planner or Elder Law Attorney before making significant financial decisions.

| State | Individual Income Limit (2026) | Individual Asset Limit (2026) |

|---|---|---|

| Most States | $2,982/month | $2,000 |

| California | No limit (Nursing Home) | $130,000 |

| Illinois | $1,304/month | $17,500 |

| New York | Varies | $33,038 |

| Connecticut | $2,982/month | $1,600 |

Once you’ve confirmed your parent’s Medicaid eligibility, proceed to Step 3 to begin the application process and explore how to combine benefits.

Step 3: Apply for Medicaid and Combine Benefits

After confirming your parent qualifies for Medicaid based on financial and medical criteria, the next step is to submit the application and coordinate their benefits. Since Medicaid is managed at the state level, you’ll need to apply through your state’s agency rather than a federal office.

How to Submit a Medicaid Application

Most states provide three main ways to apply for Medicaid:

- Online through your state’s Medicaid website or HealthCare.gov

- By mail using printed application forms

- In person at local eligibility offices or Aging and Disability Resource Centers (ADRCs)

If needed, you can designate a trusted individual, such as a family member, attorney, or friend, to handle the application process. Just make sure they have access to the necessary financial documents.

To complete the application, you’ll need to provide documentation of your parent’s identity, income, and assets. This often includes 60 months of financial records to ensure compliance with Medicaid’s look-back period rules. For long-term care applications, you may also need to submit bank statements, property deeds, and details of any asset transfers or gifts.

If your parent has unpaid medical bills from the past three months, include those as well. Medicaid may offer retroactive coverage for these expenses. While Medicaid agencies usually process applications within 45 days, it can take up to 90 days if a disability determination is involved. However, some states process applications much faster – sometimes in as little as 24 hours.

Once the application is approved, you can explore ways to integrate Medicaid with other benefits for a more seamless experience.

Consider Dual Eligible Special Needs Plans (D-SNPs)

If your parent qualifies for both Medicare and Medicaid, they are considered dually eligible. While they can keep Medicare and Medicaid as separate programs, Dual Eligible Special Needs Plans (D-SNPs) offer a simpler alternative by combining the two into a single plan. Many D-SNPs feature $0 premiums, $0 copays, and $0 deductibles for individuals with full Medicaid benefits.

D-SNPs also improve care coordination by assigning a single team to manage both Medicare and Medicaid services. This approach reduces administrative hassles and ensures better communication between healthcare providers. In 2021, about 29% of dual-eligible adults were enrolled in integrated plans like D-SNPs, Medicare Advantage with Medicaid Managed Care, or the Program of All-Inclusive Care for the Elderly (PACE).

For those who prefer community-based healthcare, PACE provides a team-based model, bringing together Medicare and Medicaid services under one group of professionals. If you’re unsure whether to stick with traditional coverage or opt for an integrated plan like D-SNPs, reach out to your State Health Insurance Assistance Program (SHIP) for personalized guidance.

Step 4: Use Spend-Down and Asset Protection Methods

If your parent’s countable assets are over Medicaid’s $2,000 limit, you can legally convert cash into exempt assets to stay within the rules. However, this must be done carefully to avoid penalties during Medicaid’s 60-month look-back period.

Spend-Down Strategies to Qualify for Medicaid

One way to reduce countable assets is by using savings to pay off the mortgage on the primary residence. Home equity is typically exempt, with limits ranging from $752,000 to $1,130,000, depending on the state. You can also invest in home improvements – like replacing the roof, upgrading HVAC systems, or adding accessibility features such as wheelchair ramps or walk-in tubs. These upgrades turn cash into exempt equity.

Other spend-down options include:

- Purchasing a vehicle (one vehicle is exempt under Medicaid rules)

- Setting up an irrevocable funeral trust (typically $7,000 to $15,000)

- Paying off existing debts

- Covering necessary medical expenses like hearing aids ($2,000 to $7,000) or dental implants

“A proper spend-down doesn’t mean wasting money; it means repositioning assets in a way that is allowed by Medicaid.” – US Law Explained

It’s crucial to keep detailed records of all spend-down activities, including receipts, contracts, and invoices.

If your parent’s income exceeds Medicaid’s limit, some states offer a “medically needy pathway.” This allows you to spend excess income on medical bills and prescriptions until you meet the state’s threshold. In “income cap” states like Alabama and Texas, you’ll need to set up a Qualified Income Trust (QIT) to make excess income exempt.

Beyond these steps, protecting joint assets becomes especially important when only one spouse is applying for long-term care.

Protecting Assets for Spouses

Federal laws include spousal impoverishment protections to ensure the healthy spouse isn’t left destitute. The Community Spouse Resource Allowance (CSRA) lets the healthy spouse keep up to $162,660 in joint assets as of 2026, while the spouse applying for Medicaid is limited to $2,000.

Medicaid calculates this allowance based on a “snapshot date”, which is the first day your parent begins a continuous 30-day stay in a care facility. To protect assets, you might:

- Convert excess funds into a Medicaid-compliant annuity for the healthy spouse

- Use savings to pay off the couple’s mortgage or make home repairs

- Pay a family member for caregiving services under a formal “Life Care Agreement” to ensure Medicaid recognizes these payments as legitimate expenses, not gifts

These strategies require careful planning, but they can help ensure your family’s financial security while meeting Medicaid’s requirements. Proper documentation and legal guidance are key to navigating this process successfully.

Step 5: Handle Approval, Appeals, and Benefit Coordination

Once eligibility is confirmed and financial strategies are in place, the next step involves finalizing Medicaid approval, addressing any appeals, and ensuring smooth coordination of benefits with Medicare.

Medicaid Approval Timeline and Process

After submitting the Medicaid application, the state typically processes it within 45 days – or 90 days if a disability determination is required. Medicaid eligibility is retroactive to the application date, so applying as soon as long-term care is needed can help your family avoid paying out-of-pocket costs during the processing period.

During this time, the state may request additional documents. It’s crucial to respond quickly to avoid delays or denial. Always keep copies of everything you submit and, if possible, get a date stamp from your local Medicaid office as proof of submission.

“The Medicaid agency usually has 45 days to process your application. If the application requires a disability determination, the agency can take 90 days.” – ACL Administration for Community Living

What to Do If Medicaid Is Denied

If the application is denied, you have the right to appeal. The denial notice will explain why the application was rejected and provide details on how to request a “fair hearing.” While state deadlines vary, federal law mandates that no deadline can exceed 90 days from the date the notice is mailed.

To appeal, submit a written request that states, “I disagree with this decision and request an appeal.” Be sure to date and sign the document, and get a date stamp when submitting it at your local Medicaid office. Before the hearing, you can review your case file to understand the evidence the state used. During the hearing, you’re allowed to present witnesses, medical records, or have legal representation.

If your appeal is successful, Medicaid coverage is usually backdated to the original application date. States are required to resolve appeals within 90 days, or within 7 days if the appeal is expedited due to urgent health concerns.

Knowing how to navigate the appeal process is vital to ensuring Medicaid benefits are secured without unnecessary delays.

Coordinating Medicare and Medicaid Benefits

For individuals who qualify for both Medicare and Medicaid, Medicare is always the primary payer. It covers services like hospital stays, doctor visits, and up to 100 days of skilled nursing care (with copayments starting after day 20). Medicaid acts as the secondary payer, covering costs such as Medicare premiums, deductibles, and copays, as well as long-term nursing home care beyond Medicare’s 100-day limit.

Dual-eligible individuals can reduce or eliminate most out-of-pocket expenses through Medicaid coverage. To simplify benefit coordination, consider enrolling in a Dual Eligible Special Needs Plan (D-SNP). These plans integrate Medicare and Medicaid benefits into a single policy. For help finding D-SNP or PACE (Program of All-Inclusive Care for the Elderly) options in your area, contact your State Health Insurance Assistance Program (SHIP).

It’s important to note that appeals for services are handled differently depending on the program. Medicare-covered services follow the federal Medicare appeals process, while Medicaid-covered services follow your state’s Medicaid-specific procedures. This step ensures that both programs work together effectively, completing the path to comprehensive long-term care coverage.

Conclusion: Get Help with ElderHonor Resources

Why Early Planning Matters

Navigating Medicare and Medicaid for long-term care requires careful planning, especially because of the 60-month look-back period. This timeframe can lead to transfer penalties if not managed properly. Given the high costs of long-term care and Medicare’s limited coverage, preparing well in advance is essential to avoid financial strain.

For the 13.7 million Americans eligible for both Medicare and Medicaid, the stakes are even higher. These individuals represent about 34% of Medicare spending and 40% of Medicaid spending. Early action ensures you can meet eligibility requirements while steering clear of penalty triggers. By planning ahead, you can use these benefits effectively and with confidence.

Use ElderHonor for Caregiving Guidance

ElderHonor is here to simplify this complicated process. Their resources, like the ElderHonor Toolkit, are designed to guide families through every step. The toolkit covers essential areas like starting difficult conversations, exploring aging in place strategies, and planning estates – all critical when managing long-term care benefits.

Additionally, personalized coaching offers tailored advice on eligibility, creating integrated care plans, and navigating the application process. These tools can help you avoid common mistakes, such as missing the look-back period or delays caused by incomplete paperwork.

For more help, visit elderhonor.com. You’ll find worksheets, assessments, and expert advice to ensure a smoother transition to dual coverage and avoid unnecessary delays in care.

FAQs

Does Medicaid pay for nursing home care after Medicare’s 100 days end?

Medicaid usually steps in to cover nursing home care after Medicare’s 100-day limit in a skilled nursing facility has been reached. While Medicare is designed to handle short-term care needs, Medicaid becomes the go-to option for long-term care once Medicare benefits run out.

What counts as an “asset” for Medicaid long-term care eligibility?

An “asset” for Medicaid long-term care eligibility refers to things like cash, bank accounts, real estate (though your primary residence might be excluded in certain situations), and other valuable items. Medicaid reviews these resources to decide if you qualify financially for their program.

Will giving money to family within 5 years affect Medicaid approval?

Yes, gifting money to family members within five years of applying for Medicaid can impact your eligibility. Medicaid examines asset transfers made for less than fair market value during the five-year look-back period. If such transfers are found, they can trigger a penalty, delaying your access to benefits until the penalty period is over. While there are exceptions to this rule, it’s crucial to carefully plan any financial gifts well in advance of applying for Medicaid.