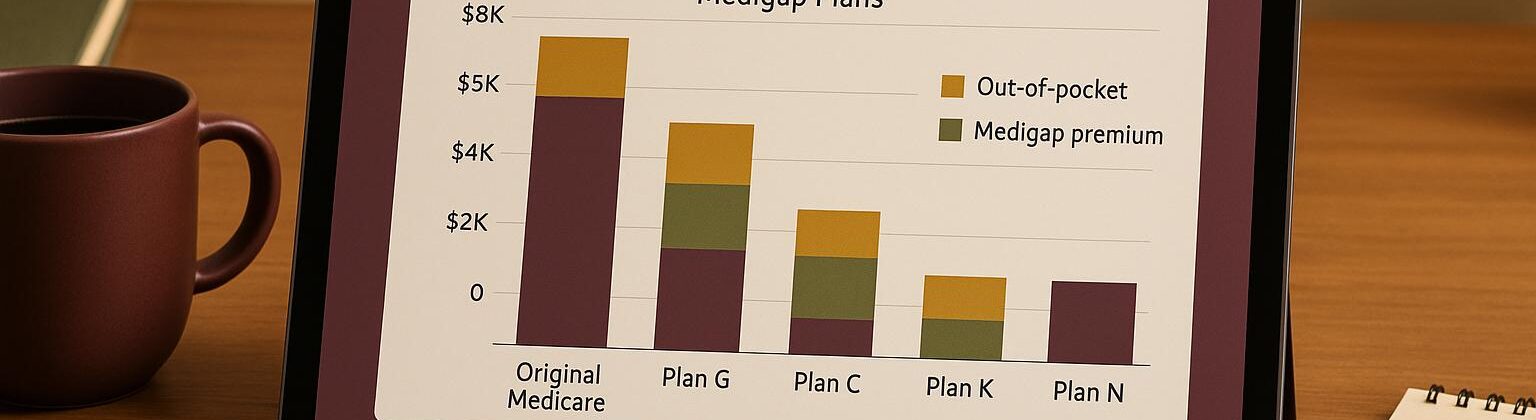

Medigap plans help cover out-of-pocket costs that Medicare Parts A and B don’t, like deductibles, coinsurance, and copayments. Two popular plans, Plan G and Plan F, offer varying levels of coverage and costs, making it essential to understand their differences before choosing.

- Plan G: Covers most expenses except the Medicare Part B deductible. It’s available to new Medicare enrollees and typically has lower, more stable premiums.

- Plan F: Offers full coverage, including the Part B deductible, but is only available to those eligible for Medicare before January 1, 2020. Premiums are higher and tend to increase faster due to its aging risk pool.

Premiums for both plans vary based on your location, age, and insurer pricing methods. Plan G is generally a better option for those seeking lower costs and predictable increases, while Plan F is ideal for those who prioritize maximum coverage and are already eligible.

| Factor | Plan G | Plan F |

|---|---|---|

| Monthly Premiums | Lower, gradual increases | Higher, steeper increases |

| Part B Deductible | Not covered | Covered |

| Availability | Open to new enrollees | Limited to prior enrollees |

| Risk Pool | Growing, younger members | Aging, older members |

| Long-term Costs | More predictable | Less predictable |

Choosing the right plan depends on your budget, health needs, and eligibility. Plan G is a solid choice for cost control, while Plan F works for those who value full coverage.

MASSIVE Medicare Supplement Rate Increases Coming

1. Plan G

Plan G is a widely chosen Medigap plan that provides extensive coverage, with just one key cost-sharing requirement. Here’s a closer look at its costs, coverage, and eligibility to help you decide if it’s the right fit for your needs.

Monthly Premiums

The monthly premiums for Plan G can vary based on several factors, including:

- Location: Where you live plays a big role in determining costs.

- Age: Older enrollees often face higher premiums.

- Provider: Different insurers set different rates.

- Pricing Method: Insurers use one of three methods:

- Community-rated: Everyone pays the same rate, regardless of age.

- Attained-age: Premiums increase as you get older.

- Issue-age: Rates are based on your age at the time of enrollment and don’t rise as you age.

Coverage Details

Plan G is designed to fill most of the gaps left by Original Medicare. It covers coinsurance, copayments, and other costs tied to hospital stays, skilled nursing care, and even emergency services abroad. However, there’s one major exception: it does not cover the Medicare Part B deductible. Once you’ve paid the Part B deductible, Plan G takes care of the rest, offering more predictable out-of-pocket costs.

Eligibility and Availability

To enroll in Plan G, you need to have Medicare Parts A and B. The best time to sign up is during the six-month Medigap Open Enrollment Period that begins when you enroll in Part B. During this window, insurers are required to offer coverage without charging higher premiums for pre-existing conditions.

For those under 65 who qualify for Medicare due to a disability, availability and pricing for Plan G can vary by state. Additionally, certain life events – like losing employer-sponsored coverage – may grant you guaranteed issue rights, ensuring you can access Medigap coverage when you need it most.

State-by-State Cost Variations

Plan G premiums differ significantly across states. Factors like local healthcare expenses, the level of insurer competition, state regulations, and even personal habits like tobacco use can all impact pricing.

2. Plan F

Plan F, once considered the go-to option for comprehensive Medigap coverage, is now only available to individuals who were eligible for Medicare before January 1, 2020. If you’re considering this plan, understanding its costs and eligibility rules is crucial.

Monthly Premiums

Plan F typically carries higher premiums compared to other Medigap plans. Why? Its extensive coverage comes at a price. Factors like your age, where you live, and the pricing method used by the insurance company all influence the cost. Since enrollment has been closed to new members since January 1, 2020, the existing pool of Plan F members is aging. This often leads to rising premiums as older members generally have higher healthcare costs.

Most insurers use the attained-age pricing method, which means premiums increase as you get older. While Plan F has historically been known for its broad coverage, this pricing structure can make it more expensive over time.

Coverage Differences

What sets Plan F apart is its unmatched coverage. Unlike Plan G, which requires you to pay the Medicare Part B deductible out of pocket, Plan F takes care of it for you. In fact, after you pay your monthly premium, you’ll have virtually no additional out-of-pocket costs for Medicare-covered services.

Here’s what Plan F covers:

- Medicare Part A and Part B deductibles

- Coinsurance and copayments for Medicare services

- Skilled nursing facility care coinsurance

- The first three pints of blood

- Emergency care during foreign travel

This level of coverage eliminates much of the guesswork when it comes to healthcare expenses, making it easier to plan your medical budget.

Eligibility and Availability

Plan F is only available to those who became eligible for Medicare before January 1, 2020. This change was driven by the Medicare Access and CHIP Reauthorization Act of 2015, which banned Medigap plans covering the Medicare Part B deductible for new beneficiaries. If you already have Plan F, you can keep it for as long as you like, and it will continue to provide the same benefits.

For those who don’t qualify for Plan F, Plan G is a popular alternative. While it doesn’t cover the Part B deductible, it offers similar benefits otherwise.

Cost Variations by State

Premiums for Plan F can vary widely depending on where you live. In states with higher healthcare costs or less competition among insurance companies, premiums are often significantly higher. For example, some states see differences of hundreds of dollars per month. Additionally, because the Plan F risk pool is closed to new enrollees, states with older member pools may experience steeper premium increases.

State regulations also play a role. Some states have stricter oversight of premium increases, which can help slow the rate of growth, while others allow insurers more flexibility. If you’re a tobacco user, be prepared for even higher premiums – surcharges of 50% or more are common in most states for those who smoke or use other tobacco products.

sbb-itb-48c2a85

Advantages and Disadvantages

When comparing Plans G and F, it’s helpful to weigh their advantages and disadvantages to make an informed decision. Plan G stands out for its lower premiums and steady rate increases, while Plan F offers near-complete coverage but comes with higher, often rising premiums.

Plan G is popular for its affordability and predictable costs. It’s available to new Medicare beneficiaries and features competitive premium rates. One of its key benefits is a fixed annual deductible, which simplifies budgeting. However, this deductible might be seen as a drawback for those who prefer not to have any recurring out-of-pocket expenses. On the plus side, because new members can still enroll, premium increases for Plan G tend to be more gradual over time.

Plan F, by contrast, is known for its comprehensive coverage. After paying the monthly premium, beneficiaries usually face little to no additional out-of-pocket costs for Medicare-covered services. However, Plan F is no longer open to new enrollees, limiting it to those who joined during its availability period. This restricted enrollment means the insured group under Plan F is older, which often leads to sharper premium increases over time.

Here’s a side-by-side comparison of the two plans:

| Factor | Plan G | Plan F |

|---|---|---|

| Monthly Premiums | Lower with competitive rates | Higher and often rising over time |

| Out-of-Pocket Costs | Includes Medicare Part B deductible | Minimal costs beyond the premium |

| Availability | Open to new beneficiaries | Restricted to prior enrollees |

| Risk Pool | Growing due to new enrollees | Older group, leading to higher risk |

| Premium Stability | Gradual increases | Steeper increases as the group ages |

| Coverage Gaps | Limited to Part B deductible | Virtually none |

| Long-term Value | Better for cost control | Less appealing due to rising premiums |

It’s also worth noting that Plan F is unavailable to most new beneficiaries due to eligibility restrictions. Factors like location and tobacco use can affect premium rates for both plans, with Plan F often experiencing faster premium hikes.

Ultimately, Plan G is often seen as a better option for those seeking lower, more stable premiums and manageable out-of-pocket costs. Meanwhile, Plan F appeals to those who prefer nearly no out-of-pocket expenses, even if it means paying higher premiums that may increase over time. Understanding these distinctions is key to planning your healthcare budget and managing future expenses effectively.

Conclusion

Grasping the nuances of Medigap premium costs is a key step in making smart healthcare choices for retirement. Comparing plans based on both cost and coverage ensures your decision aligns with your needs and priorities.

Plan G often comes with lower monthly premiums and steadier rate increases, thanks to its open enrollment status. However, it does require you to pay the annual Medicare Part B deductible. On the other hand, Plan F delivers comprehensive coverage with minimal out-of-pocket expenses but tends to have higher premiums due to its closed enrollment pool, which includes an aging population. Keep in mind that premiums can vary widely depending on your location.

Ultimately, your choice should reflect your personal situation. If you prefer predictable monthly costs and are okay with an annual deductible, Plan G might be a better fit for the long haul. But if you value maximum coverage and already have Plan F, sticking with it could be the right move.

Weigh your current expenses against your future needs. Think about your health, how much flexibility you have in your budget, and how comfortable you are with potential out-of-pocket costs. Remember, switching plans later might involve medical underwriting, so it’s crucial to make an informed decision during your initial enrollment period.

For families juggling caregiving responsibilities, understanding Medigap costs is just one piece of the puzzle. ElderHonor offers resources, tools, and personalized coaching to help families navigate the challenges of caring for aging parents with confidence and clarity.

FAQs

How do your age and location affect the cost of Medigap Plan G and Plan F?

Your age and location are two of the biggest factors that affect the cost of Medigap Plan G and Plan F. Premiums can differ significantly depending on where you live. For instance, states like Florida tend to have higher average costs compared to places like Texas. This is largely because healthcare expenses and state regulations vary across the country.

Age also plays a big role. For example, if you’re 66 years old, the average monthly premium for Plan G is about $142. But as you get older, those rates climb – reaching much higher amounts by the time you’re 98. Plan F follows a similar trend, with an average monthly cost of $228, though the exact price depends on both your age and where you live.

These differences are also tied to how insurers calculate premiums. Methods like community-rated, issue-age-rated, or attained-age-rated impact whether your rates stay steady or increase as you age. Each pricing method works differently, so it’s worth understanding how your chosen plan is structured.

Why might new Medicare enrollees choose Plan G instead of Plan F?

Plan G is often a budget-friendly choice for those new to Medicare since it doesn’t include coverage for the Medicare Part B deductible, which is set at $257 in 2025. Even without this coverage, Plan G offers nearly the same extensive benefits as Plan F, making it an appealing option for individuals comfortable covering the deductible themselves.

Another advantage of Plan G is its availability to all new Medicare enrollees. On the other hand, Plan F is limited to individuals who became eligible for Medicare before January 1, 2020. This makes Plan G a practical and accessible option for the majority of new beneficiaries.

Why do some people choose to keep Medigap Plan F even though it has higher premiums?

Medigap Plan F remains a go-to choice for many, even with its higher and rising premiums, because it offers the broadest range of coverage among Medigap plans. It takes care of all out-of-pocket expenses tied to Medicare Parts A and B, including deductibles, copays, and coinsurance.

This extensive coverage brings predictability and reassurance, especially for those who prefer to sidestep surprise medical bills. Its straightforward nature and financial protection appeal to individuals who prioritize comprehensive coverage over cutting costs.